These Guidelines allow State aid for two purposes:

– Aid to compensate for increases in electricity prices resulting from the inclusion of the costs of greenhouse gas emissions due to the EU ETS [indirect emission costs].

– Aid involved in the optional transitional free allocation for the modernisation of the energy sector.

Introduction

Certain Commission decisions are so detailed they provide very useful, step-by-step guidance on how to determine whether what appears to be a commercial transaction in fact contains State aid. The case which is reviewed in this article contains such a textbook analysis.

The case is also very unusual because the Commission, in decision SA.38145, examined alleged State aid granted by Riga airport to Ryanair after it received a complaint from the operator of the airport itself! So we have here the rather bizarre situation of the operator claiming that its arrangements with Ryanair were not market conform, while the Commission proved the opposite![1]

Background

The airport and the airport operator – designated as RIX – are both wholly owned by the state. RIX and Ryanair signed an agreement in 2004, which was accompanied by a side letter.

The Commission’s assessment of the complaint focused on the existence or not of an economic advantage in the agreement and side letter taken together.

The market economy operator test: Two methods

In order to find out whether an undue advantage had been granted to Ryanair, the Commission used the Market Economy Operator Test [MEOT]. The application of the MEOT to the air transport sector is foreseen in the 2014 Aviation Guidelines. According to point 53 of the Aviation Guidelines, there are two versions of the MEOT: the comparative or benchmarking method and the profitability method.

The first method requires a comparison of the fees charged by an airport operator with a benchmark that corresponds to market prices. However, the Commission pointed out in its decision that it “(25) does not consider that, at the present time, an appropriate benchmark can be identified to establish a true market price for services provided by airports.”

“(26) The application of the MEO test based on an average price on other similar markets may prove helpful if such a price can be reasonably identified or deduced from other market indicators. However, this method is of limited relevance for airport services, as the structure of costs and revenues tends to differ greatly from one airport to another. This is because costs and revenues depend on how developed an airport is, the number of airlines which use the airport, its capacity in terms of passenger traffic, the state of the infrastructure and related investments, the regulatory framework which can vary from one Member State to another, and any debts or obligations entered into by the airport in the past.”

“(27) Moreover, the liberalisation of the air transport market complicates any purely comparative analysis. As can be seen in this case, commercial practices between airports and airlines are not always based exclusively on a published schedule of charges. Rather, these commercial relations vary largely. They include sharing risks with regard to passenger traffic and any related commercial and financial liability, standard incentive schemes and changing the spread of risks over the term of agreements. Consequently, one transaction cannot really be compared with another based on a turnaround price or price per passenger.”

“(28) In addition, benchmarking is not an appropriate method to establish market prices if the available benchmarks have not been defined with regard to market considerations or the existing prices are significantly distorted by public interventions.”

“(29) Moreover, as the Union courts have recalled, benchmarking by reference to the sector concerned is merely one analytical tool amongst others to determine if a beneficiary has received an economic advantage, which it would not have obtained in normal market conditions. As such, while the Commission may use that approach, it is not obliged to do so where, as in this case, it would be inappropriate.” [At this point the decision cites the judgments of the General Court in cases Ryanair v Commission (Angoulême airport), T-111/15; Ryanair v Commission (Pau airport), T-165/15; Ryanair v Commission (Nîmes airport), T-53/16; Ryanair v Commission (Altenburg Nobitz airport), T-165/1]

Therefore, the Commission opted for the profitability method.

– Ad –

European State Aid Law (EStAL) provides you quarterly with a review of around 100 pages, containing articles, case studies, jurisdiction of both European and national courts as well as communications from the European Commission. EStAL covers all areas pertaining to EU State aid and subsidies, among others:

✓ The evolution of the concept of State aid;

✓ State aid Modernization;

✓ Services of General Economic Interest (SGEI);

✓ General Block Exemption Regulation (GBER);

✓ Judicial review of Commission Decisions;

✓ Economic assessment and evaluation;

✓ Enforcement at national level;

✓ Sectoral aid and guidelines.

Since profitability has to be calculated over a certain period of time, the Commission explained that it considered “(32) that the appropriate timeframe for assessing the profitability of arrangements between airports and airlines is typically the time horizon of the agreement itself.”

The relevant period in this case was from 1 November 2004 to 31 March 2015. In addition, the Commission took the 2004 agreement and the side letter to be a single transaction as they had the same objective and were concluded at the same time.

MEOT methodology: Incremental analysis

In essence, the MEOT is an analysis of incremental revenue and incremental costs generated and caused, respectively, solely by the relevant transaction. For a transaction to be market conform, the MEOT must prove that:

More specifically, the following are taken into account in order to apply the MEOT:

Incremental revenue [per accounting period]

Aeronautical revenue

A = Number of expected passengers x fee per passenger

B = Number of flights x fee per flight

Non-aeronautical revenue

C = Number of passengers x revenue per passenger [shops, parking, etc]

D = Total revenue = A + B + C

Incremental costs [per accounting period]

Operating costs

E = Number of expected passengers x cost per passenger [handling, cleaning, depreciation, etc]

Extra investment costs

F = Only when they are necessary or required investments over relevant period

G = Total costs = E + F

Net result [per accounting period]

H = D – G

Net discounted result [over whole of relevant period]

∑H/(1 + r)n = net result discounted at an appropriate rate, r, over the number of periods, n

As the Commission put it, “(41) it needs to be established whether, when setting up an arrangement with an airline, the airport is capable of covering all the costs stemming from the arrangement, over the duration of the arrangement, with a reasonable profit margin on the basis of sound medium-term prospects. This is to be measured by the difference between the incremental revenues expected to be generated by the agreement and the incremental costs expected to be incurred as a result of the agreement, the resulting cash flows being discounted with an appropriate discount rate.”

In pursuit of profit, an airport operator is not required to treat all airlines equally. “(43) Price differentiation is a standard business practice. Such differentiated pricing policies should, however, be commercially justified.”

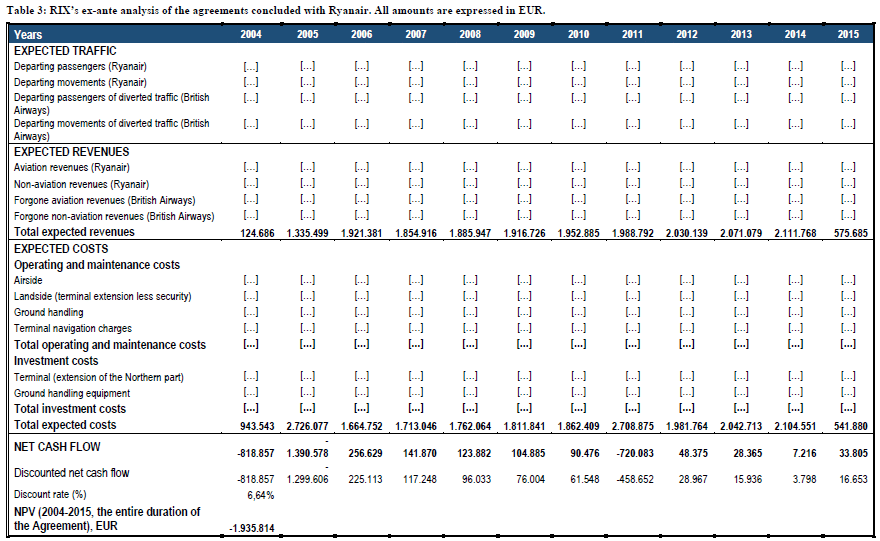

Then the Commission observed that “(45) in the present case, neither RIX nor the Latvian authorities provided a business plan preceding the conclusion of the 2004 Agreement and the Side Letter.” “(46) Upon the Commission’s request, the Latvian authorities presented a table prepared by RIX containing an overview of the incremental costs and revenues that could have been expected at the time the agreements were concluded, as summarised in Table 3”. [Table 3 is reproduced below]

“(47) Table 3 shows that RIX expected the costs stemming from the agreements to exceed the revenues, leading to a negative net present value (‘NPV’) of the incremental cash flows of EUR – 1.9 million over the duration of the agreement.”

This, of course, raises the very important question, that is not answered in the Commission decision, why the airport operator entered into a loss-making arrangement.

At any rate, what is immediately noticeable in table 3 is that it also contains presumed losses from passengers diverted away from then existing British Airways flights and from reduction of British Airways flights and also the costs from extension of the terminal. These two items can be validly included in the calculations only if they have a causal relationship with the agreement between RIX and Ryanair. And fixed costs that would have been incurred anyway must always be excluded.

Source: European Commission

Application of the MEOT

The Commission had to verify the correctness of the following:

The expected traffic generated by Ryanair.

The expected incremental revenues.

The foregone revenues related to British Airways.

The expected incremental costs [especially those possibly linked to fixed costs that could have been incurred in any case].

Traffic projections

In the absence of any explicit projections by RIX, the Commission “(50) reasonably assumed that a private operator in its planning would expect an airline to at least try to meet the minimum thresholds under the agreement in order to achieve the lowest possible passenger fee. […] The Commission accepts that it was reasonable to assume that Ryanair would achieve annually departing passenger numbers of roughly […] in 2004, […] in 2005 and […] in 2006.”

“(51) On the contrary, the assumption that traffic would remain constant at […] departing passengers per year during the whole period of the agreement cannot be assumed realistic from an ex ante point of view.”

“(52) On this basis, the Commission finds the passenger numbers provided by RIX, in particular for the period after 2006, to be too low. A higher estimate should have been used for the profitability analysis considering at least an increase of Ryanair departing passengers similar to the historical growth rate observed at RIX of 4.8%. A corresponding adjustment of the traffic assumptions, without challenging any of RIX’s other assumptions about costs and revenues, would make the agreement between RIX and Ryanair profitable over its entire duration. Using a presumed annual growth rate of 4.8%, the NPV of the agreement becomes EUR +500 000 instead of EUR -1.9 million.”

“(53) The Commission furthermore performed a sensitivity analysis based on the adjusted traffic using a more pessimistic assumption about the growth rate of traffic. The conclusion of such analysis showed that even in a more negative scenario, that is by reducing the traffic growth rate by one percentage point (to 3.8% instead of 4.8%), the agreement would still be incrementally profitable.”

“(54) Therefore the Commission concludes that RIX’s assumptions regarding traffic projections suffer from flaws and need to be corrected for the purposes of the ex ante analysis.”

Incremental revenues

The “(55) incremental revenues that a private MEO would reasonably expect from the agreements include:

aeronautical revenues from passengers and landing charges paid by Ryanair; and

non-aeronautical revenues from, for example, car parking, franchise shops, or directly operated shops.”

Aeronautical revenues

“(56) In line with Commission practice, RIX takes into account the aeronautical revenues per departing passenger and the revenues per turnaround and multiplies them with the expected departing passenger and turnaround numbers”.

“(58) In its calculation, RIX assumes a fee of EUR […] throughout the agreement. […] As stated above, the Commission agrees that a private market operator would have expected Ryanair to achieve at least the minimum threshold of departing passengers set out in the agreement and therefore finds this approach to be reasonable.”

“(59) However, the provided calculation is inconsistent to the extent that with regard to the passenger threshold of […] to be reached between 1 November 2004 and 31 March 2006, the 2004 Agreement only provides for a fee of EUR […] for the passengers carried prior to 1 April 2005 (see recital (49) above). […] As a result, the ex ante expected aeronautical revenue from the passenger fee needs to be adapted, leading to an increase in overall revenues for RIX.”

“(60) Apart from the passenger fee, RIX takes into account the ground handling fee of […] EUR per turnaround stipulated in the Side Letter. The ex ante estimate of the number of turnarounds is derived from the ex ante estimated number of passengers, assuming a load factor of 80% and taking into account that Ryanair operates Boeing 737-800 aircraft (as stipulated in the 2004 Agreement) with 179 seats. The Commission finds this approach to be sound.”

“(61) RIX submitted that under the agreement, the airport could have expected aeronautical revenues related to Ryanair of EUR […]. The Commission believes that these revenues are underestimated given the inconsistencies with regard to the traffic assumptions (see recital (52) above) and the wrong application of the passenger fee for the period from 1 April 2005 until 31 March 2006 (see recital (59) above).”

“(62) Based on the above, the Commission considers that the aeronautical revenues need to be corrected, leading to higher expected aeronautical revenues related to Ryanair of EUR […].”

Non-aeronautical revenues

“(63) Regarding non-aeronautical revenues, RIX includes revenues from shops, restaurants, and parking, based on historical data, namely the average non-aeronautical revenues per passenger in 2003, which amount to EUR […]. This amount is then multiplied by the expected total number of Ryanair passengers.”

“(64) Non-aeronautical revenues are essentially proportional to the number of passengers. In fact, the activity of car parks, restaurants and other businesses situated at the airport depend on the number of passengers. The same is therefore true for the revenues received by the airport operator from these activities. The most reasonable approach for determining the projected incremental non-aeronautical revenues involves therefore determining an amount of revenue per passenger, multiplied by the projected incremental traffic. […] Although RIX based its calculations of the non-aeronautical revenues per passenger exclusively on 2003 historical data (not considering an average over a longer period in the past), the Commission finds the approach taken by RIX to be sound, since the data immediately precedes the signature of the agreements in 2004.”

“(65) RIX assumes that the annual growth rate for non-aeronautical revenues is 5%. This is higher than the expected inflation rate for Latvia of 3%. In light of the expansion plans of the airport (hereby likely increasing also the number of shops, restaurants and other businesses at the airport), the Commission considers this growth rate to be a conservative, yet reasonable, ex ante estimate.”

“(66) RIX estimates that the revenues from non-aeronautical activities amount to EUR […]. However, the Commission considers that there should be corrections regarding the traffic projections. Namely, when correcting for the higher ex ante traffic forecast (see recital (52) above), the Commission finds that the non-aeronautical revenues could have been expected to be higher, namely EUR […].”

We see that traffic forecasts are very important. If traffic growth is not calculated correctly, then all subsequent calculations are wrong too.

Foregone revenues

The Commission rejected “(67) the argument by RIX that the loss in revenues due to the traffic diverted from British Airways to Ryanair should be considered as negative foregone revenues (both affecting aeronautical and non-aeronautical revenues).”

“(68) The Commission notes that when listing the relevant operating costs of an airport in the 2014 Aviation Guidelines, foregone revenues are not mentioned in the Guidelines as a potential category of operating costs, since new airlines starting operations and existing airlines leaving the airport can be considered as part of the normal business operations of an airport. While it cannot be fully excluded that an arrangement with an airline entails incremental costs in the form of foregone revenues resulting from reduced activities of other airlines, convincing evidence has to be provided to show that a market economy operator in the position of the airport would have taken such foregone revenues into account.”

The Commission could have added at this point that the entry of one airline does not necessarily have a causal effect on the exit of another as, in many cases, different airlines fly into an airport from different locations in the departing country.

RIX argued that the entry of budget airlines impacted on full service carriers like British Airways, Lufthansa and KLM. “(71) Having analysed the information provided by Latvia and RIX, the Commission finds that the arguments are not sufficient. RIX failed to provide evidence showing that the substitutability of Ryanair and British Airways services was considered at the time of signing the agreement or that ex ante, it had been considered that Ryanair’s presence would have an effect on future revenues obtained from British Airways.”

“(73) It should also be noted that the services and business models of Ryanair and British Airways differ considerably. Ryanair is a low cost carrier that offers no frills services and operates according to a point-to-point business model, whereas British Airways is a full service carrier that operates a hub and spoke model, using short haul flights to European destinations to support the long haul flights departing from its hub in London. Under these circumstances, there is no indication that a market economy operator in the position of RIX would have expected British Airways to divert traffic as a result of the agreements.”

“(75) For the reasons stated above, the negative foregone revenues related to diverted traffic of British Airways need to be excluded from the ex ante assessment of the agreements.”

Incremental costs

“(76) Regarding the calculation of incremental costs, according to Commission practice, all costs incurred by the airport in relation to the airline’s activities at the airport have to be taken into account. Such incremental costs may encompass all categories of expenses, such as marketing costs and incremental personnel and equipment costs induced by the presence of the airline at the airport. All costs which the airport would have to incur anyway, independently from the arrangement with the airline, are not being taken into account in the MEO test.”

Operating costs

“(77) In absence of a business plan, the incremental operating costs that were foreseeable when the agreements were signed are difficult to determine. In particular, the approach used for the non-aeronautical revenues, which involved using the airport’s total non-aeronautical revenues to determine the incremental non-aeronautical revenue per passenger, cannot be used for the operating costs. Such an approach would involve considering the airport’s total operating costs, reduced to the number of passengers, as incremental costs. However, a significant proportion of an airport’s operating costs is fixed, which means that the total operating costs per passenger are likely to be markedly higher than the incremental costs associated with the signature of a new agreement generating additional traffic.”

“(78) For its calculation of the incremental operating costs, RIX takes into account the airport’s total costs from certain cost categories called airside operating and maintenance, landside operating and maintenance, ground handling operating and maintenance costs and terminal navigation charges.”

“(84) Having reviewed the submitted information, the Commission is not convinced as regards the incremental nature of a large part of the included operating costs, in particular regarding the cost categories “airside operating and maintenance” and “landside operating and maintenance”. Whilst RIX has provided some general explanation as regards the mentioned cost categories, it has failed to provide sufficiently granular data to allow the Commission to assess whether these costs are in fact incremental costs or whether the airport would have incurred them also absent Ryanair’s operations.”

“(85) Indeed, based on the available information, the mentioned cost categories seem to include several cost items not related to Ryanair’s presence at the airport, but which are likely to resemble fixed overhead costs (such as costs related to airfield maintenance equipment, the firefighter and crisis management unit, or costs related to the maintenance of the terminal). RIX appears to be using an average cost approach, taking into account the total costs of the airport, thereby inflating the operating costs assigned to the individual agreements.”

“(89) From the submitted information it remains unclear whether the ex ante expected incremental operating costs provided by RIX were calculated per passenger. However, if the costs were indeed calculated per passenger, the same correction with regard to the expected passenger numbers as for the revenues (see recitals (51), (52), (61) and (62) above) would have to be applied to the operating costs, leading to a higher total cost estimate. By assuming a pro rata increase in the operating costs in line with the revised passenger numbers, this would lead to total operating costs over the duration of the agreement of EUR […] instead of EUR […], which does however have no effect on the overall result (see calculation performed by the Commission in table 5 below).”

Marketing costs

“(91) Since the 2004 Agreement and the Side Letter do not include specific marketing services to be provided by Ryanair or its subsidiaries, no marketing costs have been considered in the ex ante incremental profitability analysis.”

Investment costs

“(92) Besides the operating costs, RIX claims that there are investment costs related to the agreement and includes in its calculation part of the costs related to the extension of the terminal building […], as well as costs for the purchase of ground handling equipment.”

“(93) While the Commission considers that in principle investment costs can be taken into account in the ex ante incremental profitability assessment of an agreement, the link between the investment costs and the agreement has to be clearly demonstrated: objective evidence has to be provided that shows a clear correlation between the investment and the agreement in question.”

“(94) Regarding the ground handling equipment, RIX states that it needed to purchase a total of […] new units […]. However, as the equipment in question is not specific to any type of aircraft operated by Ryanair it seems realistic to assume that part of the equipment would also have been used for the other airlines, the Commission is not convinced that the full acquisition costs can be considered incremental costs to the Ryanair agreements. However, since there is no detailed evidence in the file which would enable the Commission to calculate the correct incremental investment costs of the ground handling equipment, the Commission is not making any changes to these investment costs reported by RIX in its own analysis in Table 5 below.” So here the Commission errs in favour of RIX.

“(95) Regarding the terminal building, RIX allocates […]% of the investment amount in the extension of the terminal to Ryanair based on its proportional use of floor space, amounting to EUR […].” “(97) Having analysed the information provided by Latvia and RIX, the Commission finds that the provided arguments are insufficient and that RIX has failed to provide evidence showing a clear correlation between the operations of Ryanair and the building of the terminal extension.”

“(98) On the contrary, the data provided by RIX itself clearly shows that the decision to extend the terminal was already taken in 2003 in view of the accession of Latvia to the EU and the plans to increase the number of flights towards the major EU cities. The decision to extend the airport infrastructure was therefore not directly related to the signature of the agreements with Ryanair.”

“(100) Therefore, the Commission notes that investments related to the expansion of the terminal were not specific to Ryanair but were meant to be exploited by other airlines as well.” “(102) For the reasons stated above, the Commission concludes that the attributed investment costs related to the extension of the terminal building would need to be deducted from the incremental costs analysis.”

Discount factor

“(103) For its calculations, RIX used a discount rate of 6.64%, which corresponds to the Commission reference rates and recovery rates for the 25 EU Member States (for the period 1 May 2004 until 31 December 2006). The Commission therefore finds it to be reasonable.”

The discount and recovery rate in the Commissions’ 2008 notice is base rate plus 1 percentage point. However, the reference rate that is used in profitability calculations must contain a risk margin. It is not clear whether at this point the discount rate was only correcting for inflation. For sure a higher rate of discount would have reduced the net present value of future costs and revenue and could have changed the derived results.

Profitability analysis as corrected by the Commission

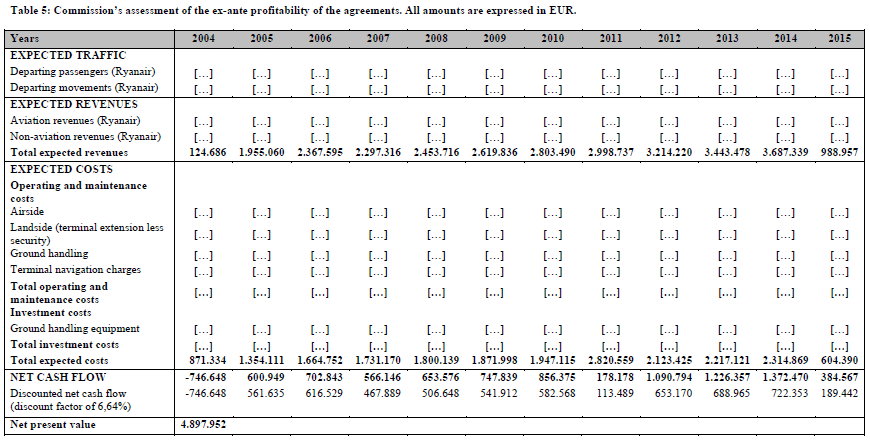

“(104) Due to the inconsistent and partially incomplete information provided by the Latvian authorities, resulting in uncertainty, the Commission has performed its own incremental profitability analysis of the agreements in question, correcting the assumptions made by RIX as indicated above. The result is summarised in Table 5 below.” [Table 5 is reproduced below.]

“(105) In its calculation, the Commission has corrected the main flaws of the assessment by adjusting the traffic forecast, the aeronautical revenues from the passenger fee, and by removing the foregone revenues and investment costs related to the extension of the terminal building, from the calculation.”

“(106) The calculation shows that when correcting these parameters, thereby accepting all other assumptions made by RIX, the NPV of the agreements is clearly positive at about EUR + 4.9 million.” “(107) The result remains positive at EUR +2.3 million when adapting the operating costs for the expected passenger numbers as described in recital (89) above.”

“(108) Since the traffic assumptions were not easily predictable, as explained in recital (50) above, the Commission has furthermore performed a sensitivity analysis taking the traffic figures provided by RIX as a given. Even with this lower traffic forecast, the NPV of the agreements remains positive at about EUR +2.4 million, which is a similar result as when adjusting the traffic projections and operating costs.”

Conclusion

The Commission found flaws in RIX’s calculations concerning:

Unrealistically low traffic projections.

Underestimated incremental revenues.

Incorrect inclusion of foregone revenue from British Airways flights.

Inflated incremental costs incorrectly linked to investment costs.

When the Commission corrected those flaws it concluded that Latvia had not granted an advantage to Ryanair that it would not have obtained under normal market conditions. Therefore no State aid was involved in the 2004 agreement.

What I miss in this case is discussion of the circumstances in which it is valid to include an appropriate share of fixed costs in the profitability analysis. A company that merely covers incremental costs without taking into account fixed costs will eventually go bankrupt. So, must an airport operator seek to recover fixed costs from other sources of revenue, such as rent from shops?

Lastly, the unanswered question is why the agreement was signed in the first place. Was the complaint an attempt by the airport operator to escape from its agreement with Ryanair? But if it was profitable, why would the airport want to do that?

[1] The full text of the decision can be accessed at: